The following originally appeared on The Upshot (copyright 2019, The New York Times Company) and is co-authored by Austin Frakt and Aaron Carroll. If you want to use the interactive features of the article, click over to the Upshot version. This also appeared on pages A12 and A13 of the print edition on August 13, 2019.

“Medicare for all” is popular, and not just among Democrats. Most Republicans favor giving people under 65 at least the choice to buy into Medicare.

But when people hear arguments against it, their support plummets. It turns out that most people don’t really know what Medicare for all means. Even asking three policy experts might yield three different answers.

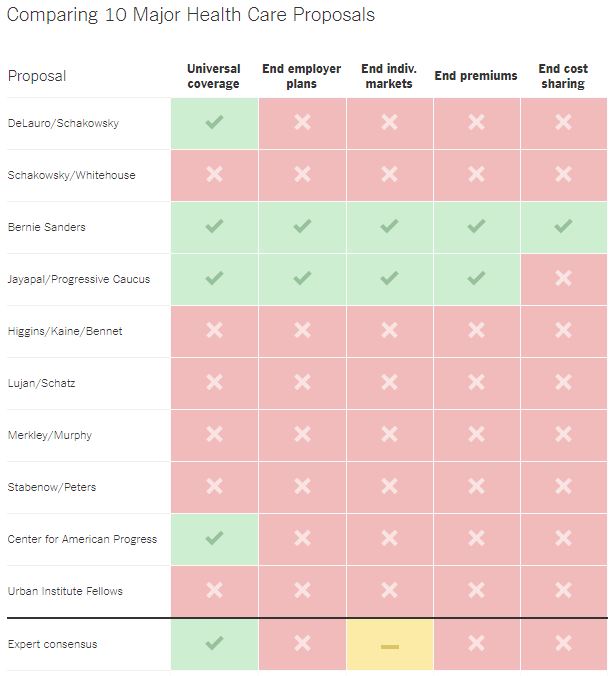

By our count, there are at least 10 major proposals to expand Medicare or Medicaid.

Some, like Senator Bernie Sanders’s bill, would create a single health care plan for all American residents. Others, like Senator Debbie Stabenow’s Medicare at 50 Act, would expand Medicare eligibility, but not to everyone. Still others would make Medicare or Medicaid a health care insurance option for many more Americans without necessarily eliminating private coverage.

Collectively the proposals vary in at least five fundamental ways, and you can vote on each category below to compare your responses with those of other readers and to see which proposals come closest to your views. We’ve also asked 11 health policy experts to weigh in on each choice. (The ideological composition of the panel spanned generally from center to left because, for now, this is a Democratic intraparty debate.)

Nearly all the experts favored universal coverage.

Universal coverage is found in every developed country except the United States, where 10 percent to 14 percent (depending on the survey) of the population is uninsured, down from a high of about 18 percent before the Affordable Care Act’s coverage expansion.

For some panelists, the decision was simple. “Universality is essential,” said Harold Pollack, a professor of social service administration at the University of Chicago. “At bottom, this is a moral issue.”

“Any decent society provides universal health care,” said Dr. Marcia Angell, a senior lecturer at Harvard Medical School.

While many Americans loathe the idea of losing choice, opting in doesn’t always work. “Some people will fail to sign up for coverage, even if it’s free,” said Sherry Glied, a health economist at N.Y.U. “People who don’t sign up may eventually need and benefit from care, and we want them to get it, so we want to make enrolling in coverage as easy as possible.”

“Universal” may not apply to everyone, perhaps leaving out undocumented residents. Some panelists favor a system in which people can opt out of coverage, which would undermine universality. There is a workaround, though, according to Dr. Ashish Jha, a physician with the Harvard T.H. Chan School of Public Health: “Asking people who opt out to pay a tax is a reasonable way to ensure that if they end up having catastrophic spending, society has a pool of funds to pay for it.”

Universality has trade-offs. It’s costly, part of why it has always faced political resistance. “Expanding coverage to a subset of the population, for example those nearer retirement age, will be cheaper and more politically palatable,” said Ellen Meara, a health economist and a professor at Dartmouth. “The desire for incremental approaches led us to create Medicare, Medicaid and the Children’s Health Insurance Program, each targeted to specific subgroups of the population.”

Ending Employer-Based Private Coverage

Most agreed that if they were starting from scratch, they would not create a system with employer-based coverage. But most also said plans that eliminate it now are politically infeasible.

Most adults under 65 get health insurance through their jobs or through a job of a working family member. Many are happy with their coverage and might rebel if forced to drop it.

One disadvantage of coverage through work is that it can cause some people to stay in jobs they don’t want. One advantage is that private coverage can offer benefits that public plans like Medicare don’t. Many other countries, even those with universal public coverage like Canada and Britain, also allow employers to offer additional coverage. “Americans like choice, and flexibility,” said Elizabeth Bradley, a public health scholar and president of Vassar College.

Other experts said it was time for employer-based coverage to go. A profusion of coverage options “generates complexity that drives up administrative costs,” said Dr. Steffie Woolhandler, a physician and a professor at Hunter College.

“We should transition away from employer-based private coverage,” Ms. Meara said.

“Employer-based coverage should be ended,” Dr. Angell said.

“From a political perspective, people with coverage from large, high-wage firms are going to be a potent force against taking it away,” Ms. Glied said.

Although he argued in favor of eliminating employer plans, John McDonough, a Harvard professor who helped write the Affordable Care Act, agreed that doing so would be politically difficult or even impossible: “It’s hard to turn around an ocean liner.”

Mr. Pollack concurred: “Any proposal to ban employer-based coverage would self-immolate.” Nevertheless, job-based coverage has some undesirable features. “Employers typically lack the bargaining power with providers to really discipline prices or health care delivery,” he said. “And the tax subsidization of employer coverage is regressive.”

Dr. Don Berwick, a senior fellow at the Institute for Healthcare Improvement, sees a way to meld work-based coverage within a single-payer system. “If employer-based coverage is retained, that does not make a single-payer approach impossible,” he said. “Employers could contribute to the single, common payment pool, as they do today to premiums for private plans.”

Replacing Individually Purchased Private Coverage

Mixed

One major objective of the Affordable Care Act was to give a reasonable option to people who didn’t qualify for public programs and could not obtain employer-based coverage. Medicare also has an individual market, through Medicare Advantage — private plans that offer alternatives to the public and traditional Medicare program.

“Having choices among plans, with insurers competing to provide plans that meet enrollees’ needs, can be a driver of innovations in benefits that respond to consumer demand, improved quality and lower premiums,” said Kate Baicker, a health economist at the University of Chicago.

Ms. Meara concurred with these advantages, but brought up a key problem with an individual market with many competitors: “Variation across health plans in approaches to quality and costs can translate into a hassle for doctors, hospitals and other health care providers.”

She pointed out that the large variety of payers in the U.S. system had led to over 1,700 distinct quality measures and a wide variety of billing requirements.

A reason to have both public and private options in one market is to provide choice. “For a country as large and diverse as ours, a single plan for all would be unworkable,” Dr. Jha said.

Yet for some, the downsides overwhelm the value of choice. “Individually purchased private coverage, like job-based coverage, generates inequality and complexity,” Dr. Woolhandler said.

“I would prefer a single-payment system more like traditional Medicare for everyone,” Dr. Berwick said. “It would not be a perfect solution at all, but it would have the enormous advantage of simplicity and lower transaction costs.”

The A.C.A. marketplaces are quite different from Medicare Advantage, though both are individual markets. Details matter, our experts said.

“In part, the marketplaces struggle because we didn’t throw enough money at them,” Mr. Pollack said. “Medicare Advantage is a much better experience, largely because both parties have collaborated to support it with generous subsidies. And less competitive Medicare Advantage market areas have the backstop and competition provided by traditional Medicare, a public option for seniors.”

Eliminating Premiums

Most of our experts saw a role for some premiums, in some cases because they thought a “no premiums” approach was politically unrealistic.

Americans are accustomed to paying at least some of the premium of a health insurance plan, although some people on Medicaid or with A.C.A. marketplace coverage pay none.

Dr. Woolhandler argued for a fully tax-financed system: Everyone could be automatically covered “whether or not they’re able to (or remember to) pay their premiums.” Additionally, “using the existing tax collection system is far more efficient than setting up a duplicative apparatus to collect premiums.”

Dr. Berwick said: “Moving to tax-financed health care makes the most sense logically. One advantage of a tax-funded system is the opportunity to engage in socially progressive financing, with wealthy people bearing a greater share of the costs.”

Ms. Bradley said “a mix is likely necessary.”

Paul Starr, a professor of sociology and public affairs at Princeton, favors tax financing, but a look at the numbers convinced him that it was not realistic. If taxes were to replace all private premiums as well as out-of-pocket spending (as in some single-payer plans), the government would have to nearly double what it now collects in personal income tax. “There’s no precedent in American history for a tax increase of that magnitude,” he said. “It’s not going to happen.”

Mr. McDonough reminded us that when Vermont considered a tax-financed single-payer system, sticker shock killed it. The required tax increase “was recognized by then-governor and single-payer champion Peter Shumlin as political suicide.”

Ms. Meara and Dr. Jha pointed out that premiums become necessary once you allow some choice in coverage through markets. More generous coverage is more expensive and would warrant some premium payment.

Finally, Ms. Baicker thought tax financing should be focused on low-income people: “My preference would be to have public programs that focus on lower-income populations, rather than using taxpayer dollars for high-income people who could afford coverage on their own.”

Eliminating Cost Sharing for Everyone

All but two of our panelists supported some type of cost sharing.

In addition to premiums, most Americans are accustomed to paying for some health care through deductibles and co-payments. High deductibles have become one of the biggest criticisms of A.C.A. plans.

Most of the panelists and most of the proposals would keep cost sharing, but Dr. Woolhandler and Dr. Angell preferred to eliminate it. “There should be no co-payments or deductibles,” Dr. Angell said.

“Cost sharing penalizes the sick and poor, who forgo vital as well as unneeded care, and suffer grave financial harms,” Dr. Woolhandler said. “Experience in some nations proves that cost sharing is not necessary to control costs.” On the contrary, she argued, collecting co-payments and deductibles just adds a costly, administrative burden.

A downside of cost sharing is that it “can lead to patients and families delaying necessary care or skimping on prevention,” Ms. Bradley said.

Ms. Glied articulated a common sentiment among many of the experts we interviewed: “Co-pays deter excessive use of the system, but the biggest effects are moving from zero to something.”

If that “something” is too big, it is “effectively just a tax on those with pre-existing conditions.”

“So the design of cost-sharing, like any incentive scheme, must be carefully considered so that it reduces overuse without limiting necessary care,” Ms. Bradley said.

This, known as value-based insurance design, was favored by many experts, including Ms. Meara, Ms. Baicker, Dr. Jha and Dr. Berwick.

We acknowledge that there are other key variations beyond these five big questions, like which benefits are covered and whether and how the government might regulate health care prices. There are also plenty of nuances among the proposals (which we hope to follow up on).

Some plans, including the one offered by Senator Sanders, as well as the Medicare for America Act, backed by Representatives Rosa DeLauro and Jan Schakowsky, would provide universal coverage. Others, like the Healthy America Program from fellows at the Urban Institute, would not necessarily do so.

Most proposals would retain employment-based coverage and individual markets. These include Medicare X (Representative Brian Higgins, Senator Tim Kaine, Senator Michael Bennet); theChoice Act (Ms. Schakowsky, Senator Sheldon Whitehouse); and the Choose Medicare Act (Senators Jeff Merkley and Chris Murphy).

Most plans would also keep premiums, though some would have subsidies for low-income families. But a few, including from Representative Pramila Jayapal and the Congressional Progressive Caucus, would do away with premiums entirely.

Almost all proposals would keep cost sharing, with some shedding it for those below the poverty threshold.

Medicare for all is not the only way to achieve major coverage expansion. Several panelists, including Ms. Glied and Mr. Pollack, like the idea of a public option or federal fallback plan — perhaps a Medicare-like plan that competes with other, private coverage. A proposal from the Center for American Progress includes versions of this idea.

Ms. Meara suggested a related idea, similar to one that Representative Ben Ray Luján and Senator Brian Schatz have proposed: “A more realistic path would make some basic set of benefits available — like a Medicaid buy-in — leaving open a path for those wishing to spend more to do so.”

Mr. Starr said the next Democratic president would not repeat the mistake of exhausting his or her political capital on health reform. Mr. McDonough agreed, saying coverage expansion debates have a way of “sucking up all the political oxygen.” He would like to see “space for consideration” on education, taxes, climate change, ethics and campaign finance reform, “and so much else.”

If Democrats win in 2020, there is sure to be a tension between ideas reflected in Dr. Woolhandler’s declaration that “health care is a human right” and Mr. McDonough’s warning that pursuing a fully government-run Medicare for all might “pre-empt progress on everything else.”

Marcia Angell, former editor of the New England Journal of Medicine, and senior lecturer in the Department of Global Health and Social Medicine at Harvard Medical School

Panel of Experts

Kate Baicker, a health economist and dean of the University of Chicago’s Harris School of Public Policy

Don Berwick, former administrator of the Centers for Medicare and Medicaid Services, and president emeritus and senior fellow of the Institute for Healthcare Improvement

Elizabeth Bradley, a public health scholar, president of Vassar College and a professor of science, technology and society

Sherry Glied, a health economist, and dean and professor at the Wagner School of Public Service, New York University

Ashish Jha, physician and director of the Harvard Global Health Institute, and professor at the Harvard T.H. Chan School of Public Health

John McDonough, former Senate staffer involved in writing and passage of the A.C.A. and professor of practice, Harvard T.H. Chan School of Public Health

Ellen Meara, a health economist and the Peggy Y. Thomson professor of evaluative clinical sciences at the Dartmouth Institute for Health Policy and Clinical Practice

Harold Pollack, professor of social service administration, University of Chicago

Paul Starr, professor of sociology and public affairs, Princeton University

Steffie Woolhandler, a primary care doctor, a distinguished professor at Hunter College, and a lecturer in medicine at Harvard. She co-founded Physicians for a National Health Program