In a post I recommend you read in full (it’s not long), Ross Douthat puts a valid question on the table: by what metrics ought we judge Obamacare? He then goes through some possible enrollment, cost, and outcomes metrics that (some) supporters really did claim would be improved by the law. He ends with something of a proposition:

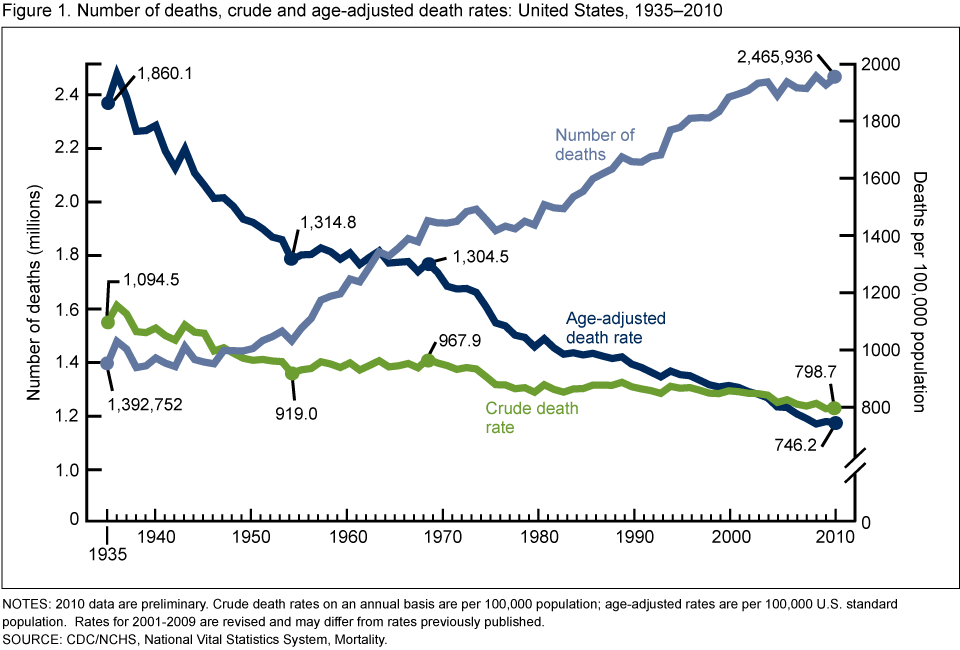

I’ll lay down this marker for the future: If, in 2023, the uninsured rate is where the C.B.O. currently projects or lower, health inflation’s five-year average is running below the post-World War II norm, and the trend in the age-adjusted mortality rate shows a positive alteration starting right about now, I will write a post (or send out a Singularity-wide transmission, maybe) entitled “I Was Wrong About Obamacare.”

It is fair to hold Obamacare supporters accountable for their claims. And I don’t think Douthat is wrong that the administration and its surrogates made the claims he lists. I just don’t, personally, think those were all reasonable claims to have been made. Many of them, and much of the debate, is far more politically salient than policy relevant. Correspondingly, my set of metrics for judging policy success would be (is) different.

Enrollment. Douthat draws on CBO projections of enrollment and reductions in uninsured as benchmarks of success. There are two problems with this. First, CBO projections are not designed to be aspirational. To be sure, one can take them up as such—and the administration did so—but that was not wise, in my view.

That leads to the second problem. Overall enrollment is a lousy benchmark, because it doesn’t tell you anything about the stability of the program at the level at which it matters: state-level markets. (I’ll get to reduction in uninsured below.) For state-level insurance markets to function, what’s needed is a mix risk that’s not too far off what insurers expected and for which they priced products. This is necessary for state-level market stability, which is a good policy metric. Related, one would like to see a “good” level of competition in exchanges, with more than a few insurers participating and dominating. My economist colleagues in industrial organization can devise myriad, decent metrics for this, none of which rely on a national, total enrollment figure.*

The cost curve. Again, Douthat is right that claims were made about cost reductions. And, again, I think it was unwise to have made them, just as it’s unwise to claim that the recent downturn in health care cost growth can be attributed to Obamacare or will continue. Fundamentally, nobody knows how to, reliably and in a politically viable and sustainable way, reduce health care costs long-term. To its credit, the ACA is chock full of experiments in cost control that, in my view, are worth a try (as are others). But to confidently predict they will succeed is to be oblivious to the lessons of the history of health care in America.

Health outcomes. Here, I think we can be more confident. I do expect insurance coverage to improve health, as the preponderance of credible evidence suggests it does. (I will have more to say about this next month.) In judging whether it does so, we should be careful to measure Obamacare’s effects relative to our best estimate of the counterfactual of no reform, not with a simple pre-post estimate, as Douthat suggests. Controlling for potentially confounding factors (e.g., economic change) is crucial. Moreover, some health outcome improvements, like mortality, may take years to manifest.

But notice that even if Obamacare does not reduce mortality (as studies suggest it will), it’s important to also consider morbidity more generally, including mental health. Broadly, I’m very confident health insurance does and will improve health outcomes. What this means is that I would not declare failure if we, to my surprise, don’t find a mortality effect, so long as we find other, worthwhile health effects.

Other good metrics. As I’ve written before, achieving “near” universal coverage is not a good metric. The ACA is simply not designed to do that, as the CBO has articulated (see the discussion on page 5 of their recent report). It cannot achieve anything like universal coverage without a massively bigger individual mandate penalty or equivalent inducement. Instead, I propose as a better metric achieving near universal access to affordable coverage of good quality. This is really what the ACA is about, despite the rhetoric. Notice that one can debate what “near universal,” “affordable,” and “good quality” mean. I’m not aware that the administration or other vocal proponents of Obamacare have established metrics along these lines; they should.

But, thanks to the Supreme Court’s ruling that states can decline to expand Medicaid without losing all federal Medicaid funding, the ACA has already failed in this regard (or states have failed it). Access to affordable coverage is unavailable for below-federal poverty line residents of states not expanding Medicaid. This is a serious policy issue that deserves a lot more attention than whether or not more than 6 or 7 or 8 million people have enrolled in exchange plans to date.

Another good metric is increase in financial protection (e.g., fewer bankruptcies) that coverage expansion might provide. We really ought to see some movement in this area.

Finally, one must acknowledge that a lot rides on what future policymakers do. Will they redirect subsidy spending for other purposes, making insurance less affordable? Will they expand Medicaid or permit states more flexibility to do so? It’s not fair to view the ACA as static policy. It’s already changed, by virtue of administrative, judicial, and congressional action. Any big program will fail if it’s not nurtured, supported, and tweaked as required.

Stepping back, fundamentally we know the ACA will fail in the sense that there’s obviously a lot more work to be done in improving the U.S. health system. Nobody should feel complacent because coverage became X% cheaper, on average or Y% of exchanges are stable with good levels of competition or morality rates fell by Z% over N years. It’s absolutely fair to ask proponents to define how to judge if the ACA is a step in the right direction, but even if it proves to be so, it’s not enough. It’s never enough. Even those who espouse benchmarks that the ACA or its tweaked successor surpasses would be wrong to claim “mission accomplished.”

In that sense, we all may be at least a little wrong about Obamacare.

* I’m dodging a complexity here. Market structure is, in fact, more complex than “state-level.” Plans can offer products on a county-by-county basis, so there’s really a patchwork of overlapping markets to consider, as one sees in Medicare Advantage.

{kind=link}

{kind=link}