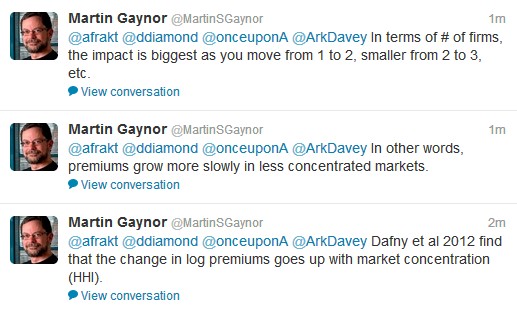

Marty Gaynor held office hours on Twitter (@MartinSGaynor) this afternoon to address this question. Here’s a screenshot of his tweets. (Read from bottom up.)

Here are those references:

UPDATE: Apparently, Gaynor wasn’t done.

Maybe he’ll keep going. You can scan his Twitter feed to find out.