Can we all calm down about death spirals? Yes, recent HealthCare.gov news has been dismal at best. Yes, the administration is statutorily locked in to the open enrollment period. And yes, if glitches persist, they may opt to delay the individual mandate through the hardship exemption. This is less disastrous than it sounds.

I’ve argued in the past that delaying the individual mandate for a year wouldn’t provoke a full death spiral; it would be an uncomfortable hiccup, but it’s not enough time for the whole market to unravel. More importantly, there are deep-in-the-weeds protections baked into the Affordable Care Act: risk adjustment, reinsurance, and risk corridors.

These programs—collectively called the “three Rs”—aid insurers if they wind up enrolling a population that is sicker and more expensive than projected. They do a crucial bit of policy work: we want plans competing on efficiency and quality, not their ability to attract the healthiest patients.

The programs have related functions, but risk corridors will play the biggest role if the individual mandate does get delayed. Their entire purpose is to stabilize premiums during the first three years of Obamacare, when it’s especially difficult for insurers to price plans.

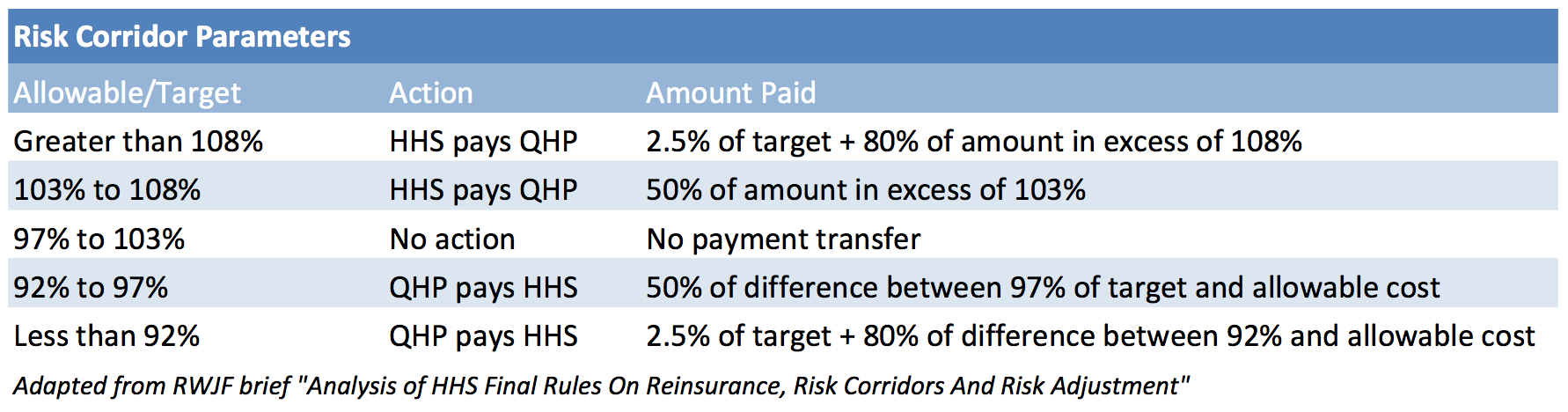

Here’s how it works: exchange plans (QHPs) projected how much their risk pool would cost overall in 2014, their “target” cost. If they’ve significantly miscalculated—or, say, if a mandate delay causes adverse selection that they couldn’t have predicted—HHS will take action:

The risk corridor mechanism compares the total allowable medical costs for each QHP (excluding non-medical or administrative costs) to those projected or targeted by the QHP. If the actual allowable costs are less than 97 percent of the QHP’s target amount, a percentage of these savings will be remitted to HHS (limiting gain). Similarly if the actual allowable cost is more than 103 percent of the QHP’s target amount, a percentage of the difference will be paid back to the QHP (limiting loss).

Total transfer depends on how badly the insurer miscalculated:

Basically, today’s worst-case scenario is that HealthCare.gov takes months to fix and the mandate is delayed until 2015, resulting in widespread adverse selection. Insurers wouldn’t recoup all losses, but the risk corridor program provides their bottom line with a substantial buffer. Importantly, it doesn’t need to be budget neutral; if the math demands it, the government can pay out more than it collects through the program. This could be expensive—the CBO scored the health law as though risk corridors were budget neutral—but it could also be offset by foregone subsidies.

Insurers have a stake in Obamacare’s success; that doesn’t magically disappear if 2014 enrollment is rockier than anticipated. The the risk corridor program continues through 2016, which would allow plans to weather 2014’s uncertainty and probably keep the following year’s premiums relatively unchanged as the risk pool normalizes.

The real risk of delaying the individual mandate is long-term political fallout from Obamacare being labeled a “fiasco”, not the dreaded insurance death spiral.

Adrianna (@onceuponA)